In order to increase revenue, brands must increase the speed with which their products move across the distribution chain from the warehouse to the shopper’s basket. This makes increasing sales velocity a leading priority to empower FMCG growth. However, cash payments are one of the biggest barriers to doing business for FMCGs across emerging markets, reducing sales velocity and increasing expense as brands, distributors, and retailers spend extra time and money processing and reconciling cash.

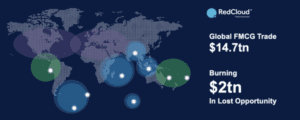

Managing and processing cash reportedly costs FMCGs and distributors between 2 to 9% of their total revenue and retailers and merchants lose between 4.7 to 15.3% per transaction. In addition, cash is slow to reconcile while digital payments are received instantly. Despite these losses, cash payments and transactions still reign across the developing world, with over 50% (19 trillion) of the $34 trillion global payments made by Micro, Small, and Medium Retailers (MSMRs) made in cash. This situation persists despite the numerous efforts made by brands, governments, and other industry players to reduce the use of cash and digitalize payments.

The reality of cash payments

Cash payments remain prevalent across the developing world because retailers want it. It’s convenient, instant, and accepted everywhere, which makes it preferable. This poses a problem to brands and distributors, as most digital payment solutions don’t have the same widespread acceptance, therefore, merchant adoptions of digital payments remain extremely low.

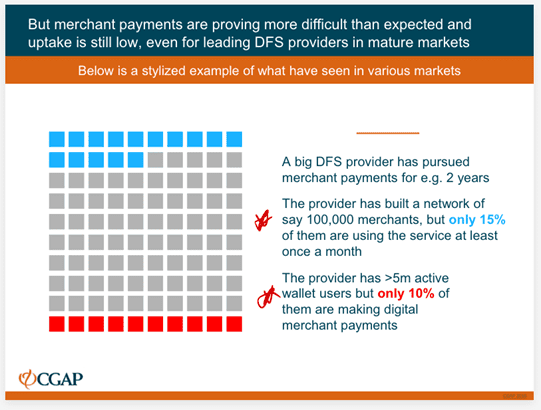

In many cases, an attempt by FMCG brands and distributors to solve the cash problem follows this pattern:

- Brands discover how much is lost through cash handling.

- To fix this problem, a digital payment solution is created, either built in-house or in partnership with a third-party payment provider.

- The payment platform is then rolled out to merchants, and sales & marketing teams are tasked with getting merchants to sign up to use the platform.

Merchant acquisition is low, with less than 10% of merchants using the platform consistently, making it cost-inefficient

Every day, similar scenarios play out across the world, from Latin America to Africa and Asia. A large FMCG in Argentina that I have spoken to, hires delivery trucks that move around every day, transporting substantial amounts of cash to a central warehouse for processing and reconciliation. This a huge concern, as the cost implications are enormous. Even the most conservative estimates put cash handling costs at 2% of total revenue, which means that an FMCG that processes $300 million worth of business annually loses $6 million to cash payments.

The retailer lynchpin

A critical look at the state of cash payments in the CPG industry shows that merchant adoption is crucial to the success of any payment digitization process. Unfortunately, many retailers still prefer to use cash for cultural and historical reasons and don’t have any incentive to switch to digital payments.

While retailers lose a significant amount of money due to cash handling, these costs are hidden and hard to identify, making cash payments seem preferable. The three main reasons I have identified as to why retailers are not transitioning to digital payments are:

- Digital and financial literacy: Retailers and merchants in developing economies have been using cash for generations. Switching to digital payments requires a new way of thinking about money. In addition, adopting a digital payment platform means learning how to use new technology, which can be off-putting for merchants who are not tech-savvy.

- Trust in payment providers: Digital payments require that retailers trust the payment provider with the security of their funds. However, many merchants aren’t aware of the security measures in place to protect their funds and are sceptical about placing their business funds in the hands of an unknown third party. This makes it a battle to get a high adoption rate for digital payments.

- Hidden cost of cash revealed: Most digital payment platforms charge transaction fees, which can seem expensive to an average retailer. Merchants may resent the fact they are being charged to use their own money where previously these costs have been hidden.

Brand-retailer partnership is the solution

Solving the cash payments problem can only be accomplished when brands partner with all the players along the distribution chain. Distributors and merchants along the chain must:

- Sign up for the same payment service/platform (acquisition)

- Have an incentive to use the payment service (value to all players on the chain)

- Remember to use the service (top of mind)

- Know how to use the service (digital & financial education)

- Be willing to pay for the service

Building this partnership is accomplished in 3 ways:

- Driving digital and financial literacy via customer success teams and initiatives.

- Providing specific incentives that encourage merchants to adopt and continue using digital payments. These include access to financing and targeted trade promotions from brands.

- Integrating digital payments with an open commerce platform that unlocks the value of the distribution chain with advantages like real-time data and insights into consumption patterns, market intelligence to help drive sales, and automated communications to reduce order processing time.

The old way of throwing an app at merchants to solve the cash problem has proven not to work in the long run.

An advantage of switching to a digital payment system is the access to financial services such as supply chain financing, loans, and other credit facilities. Access to finance remains one of the biggest obstacles to growing their business for many MSMEs, with the credit gap for MSMEs estimated at $5 trillion, 1.3 times the current level of MSME lending. Relying on cash payments means there are no accurate records or credit history, which prevents businesses from accessing financial services. Digital payments build upon financial records, which can be collateralized to access credit facilities.

Digitalize your distribution chain to solve the cash problem forever

Digitalizing the entire distribution chain is the only way brands can permanently solve the cash payment problem. Instead of building stand-alone digital payment platforms that never get adopted, what you need is an integrated commerce platform that unlocks the value of the entire distribution chain.

By opening new communication channels with merchants, providing credit facilities, and providing real-time market insights that can help businesses grow, merchants will see the advantages of digital payments, leading to widespread adoption. This is will in turn lead to faster payments, increased sales velocity and more revenue for FMCG brands.

RedCloud has built the world’s first integrated open commerce platform solves the cash problem with an integrated payment system. In addition, we also unlock the entire distribution chain and deliver value to brands, distributors, and retailers with access to real time data and insights that support strategic decisions. This increases the sales volume and frequency for all players across the chain, leading to true business growth.

Merchants who already use RedCloud have reported a 40% increase in business and are willing to recommend it to other merchants. This positive engagement with existing merchants helps to increase the adoption of digital payments through recommendations and repeat business. By partnering with RedCloud, FMCG brands can reduce costs and increase revenue by up to 25%*, a true win-win for everyone in the CPG industry.

In my next blog, I will be discussing the hidden costs of money and how retailers are losing up to €80 billion globally to cash payments.

*Statistic based on research conducted by Oliver Wyman.

â€