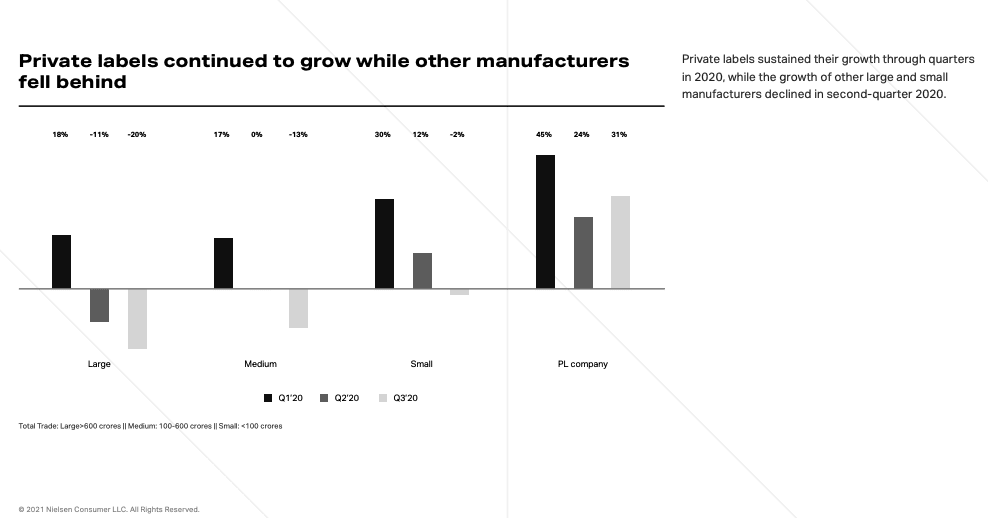

Early in the COVID-19 crisis, many large FMCG brands disappeared from stores due to panic buying and pantry loading, leading to many shoppers opting to buy private-label goods, and have continued to do so. Private label products have experienced rapid growth in the last few years, especially in emerging markets like South Africa, which reported a startling double-digit growth of 27.2 percent between March 2019 and March 2020. On the other hand, major FMCG brands experienced slow revenue growth of 1.0 percent in the CPG industry, with their market share falling by 0.6 points to 46.6 percent, while private labels and the smallest manufacturers increased their market share to 15.6 percent and 9.7 percent, respectively.

To compete favorably, larger FMCG companies need a new playbook to prevail over smaller, nimbler opponents.

Why private labeled products are on the rise

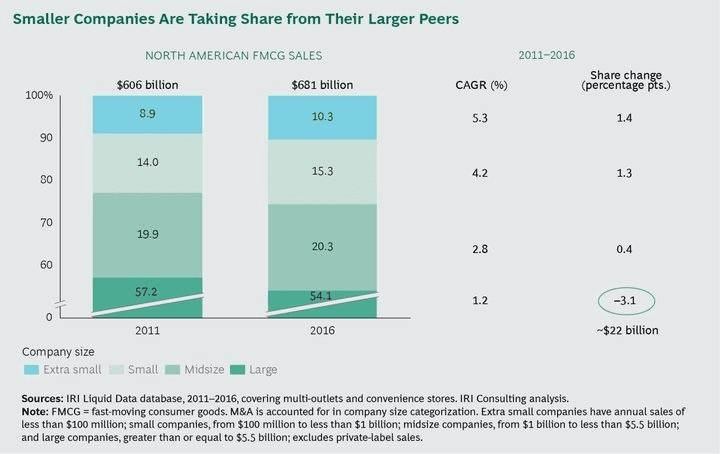

In the last few decades, large FMCGs strengthened their brands, expanded their portfolios, and created strong shareholder value in an era of big media, big retailers, and big brands. However, as recent as five years ago, smaller manufacturers began to take market share from large brands, a trend that has continued in both developed and emerging markets.

Here is a look into the factors driving the success of smaller brands and private labels:

Shifting consumer behavior and buying preferences

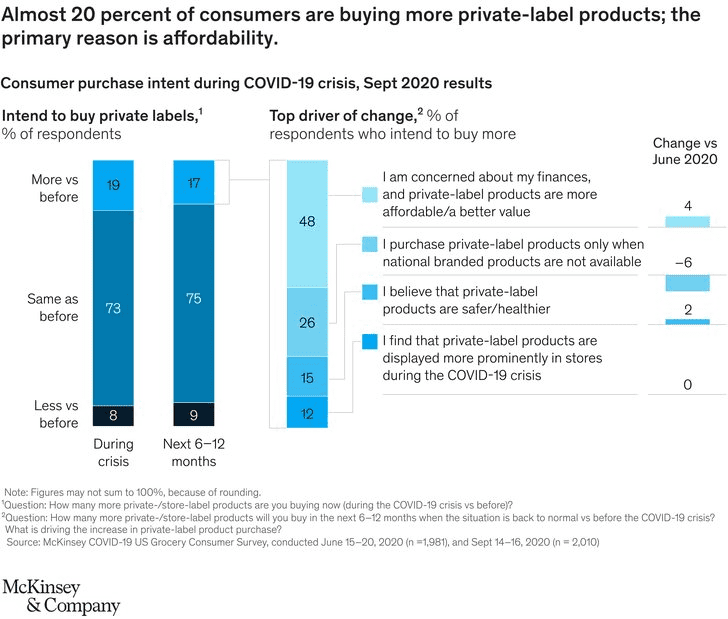

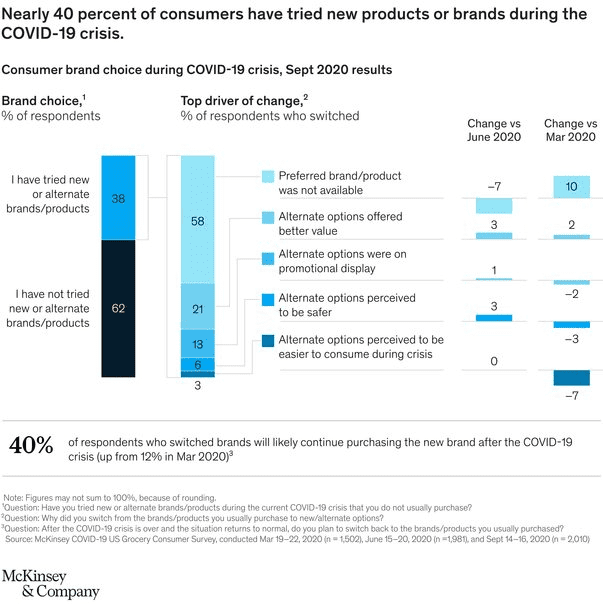

The pandemic revealed that consumers are quite willing to change their buying behavior, with customer surveys showing that 40% of customers have tried new products or brands since the start of the COVID-19 crisis. Much of this behavior was spurred by the affordability of private label brands, as customers continued to hunt for cheaper products due to the prolonged economic uncertainty.

The second-most cited reason by consumers for switching to private label brands was the unavailability of major brands as manufacturers struggled to meet rapid spikes in demand for their products.

Ease of coordination

Smaller FMCG brands can often act quicker and more creatively than their larger counterparts as they are focused and more efficient and do not bear the coordination and governance costs of large organizations. This agility and simplicity allow them to outmaneuver larger, siloed FMCG companies, ensure their products are readily available, competitively priced, and more attractive to retailers and consumers.

Expanded distribution options

Private labels have benefitted in the last few years and over the course of the pandemic, as they could manage their distribution chain and address stock shortages better than larger FMCG brands. While smaller manufacturers were previously limited to distributing their products through big retailers who carried both major brands and private labels, they can now distribute their products through multiple channels. The rise of modern trade and e-commerce now allows smaller brands to reach customers just as effectively as larger brands can, as shelf space is unlimited at online stores, and brands regardless of size, have the same visibility.

These new, digital-enabled channels also provide small brands with access to data and insights that even large FMCG brands do not have. Smaller private label manufacturers can see who is buying their products via online retail channels, send campaigns and promotions tailored to specific customer segments, and track the success of said campaigns in real-time, an ability that many marketing leaders in large FMCGs currently lack.

The above-mentioned factors combine to make private labels more attractive to retailers, which has proven to be a problem for large FMCG brands as they continuously lose market share and brand value to these smaller brands. However, large brands can take back control by digitally transforming their supply chain to become more agile and resilient.

Take back control with Red Cloud

Conventional wisdom says that large FMCG brands have few options to combat the growth of small brands and that organic growth is over, but we disagree. While consumers’ tastes may have changed, their underlying needs and desires have not. FMCG brands must now:

- Analyze demand rather than customers alone: By analyzing consumption across various geolocations rather than just customers, brands can derive valuable insights into the key demand drivers and what must be done to capture said demand. The data on this type of market segmentation shows that brands that can best meet critical customer needs will outperform alternatives in the market and reignite growth.

- Improve engagement with channel partners: Large FMCG brands who have long been unable to effectively engage with distributors and retailers due to the fragmented distribution chain must now embrace digital tools that provide affordable personalization capabilities to engage and incentivize channel partners at scale. Personalized customer engagement across multiple channels can yield up to 287 percent higher purchase rates and increase retailer satisfaction by over 600%.

This is what RedCloud, the world’s first open commerce platform provides. With RedCloud, FMCG brands can now unlock the full power of their distribution network by connecting brands, distributors, and retailers on a single platform. FMCGs can also collate valuable, actionable data at POS from every merchant in their network, providing unprecedented visibility across the distribution chain. RedCloud also analyses the data to provide easy-to-understand insights that sales and marketing leaders of large FMCG brands can leverage to understand their customers better, create targeted, retailer-specific promotions that drive sales, increase revenue, and win market share from private labels and smaller brands.

Schedule a demo today to discover how RedCloud is partnering with FMCGs across emerging markets, empowering them to sell smarter, buy better, and pay simpler.

â€