In emerging markets today, over 2 billion people and 200 million businesses lack access to savings and credit, as they are excluded from the formal financial system. Transactions are exclusively in cash, and there is no access to credit beyond informal lenders and personal networks. There is a massive gap between the credit micro, small, and medium enterprises (MSME) need and the credit facilities available to them, with studies estimating this credit gap at approximately $5 trillion, or 1.3 times the current lending level.

Despite this enormous gap, MSMEs remain crucial to emerging economies, as two out of every three full-time jobs in developing economies are provided by SMEs. The informal sector also provides employment to over half of the labor force and is at least 35 percent of GDP. Therefore, closing the credit gap and empowering MSMEs with access to credit is crucial to increasing GDP and driving economic growth.

Digital finance can close the credit gap and provide access to financial services for over 1.6 billion people in emerging economies, and provide over $2.7 trillion in new credit for MSMEs by 2025. The potential economic impact of digitizing financial services is enormous, though it varies significantly based on a country’s starting position. Lower-income countries can add 10 to 12 percent to their GDP by 2025, while middle-income countries can add up to 5 percent to their GDP by adopting digital financial services.

Close the credit gap with digitized payments

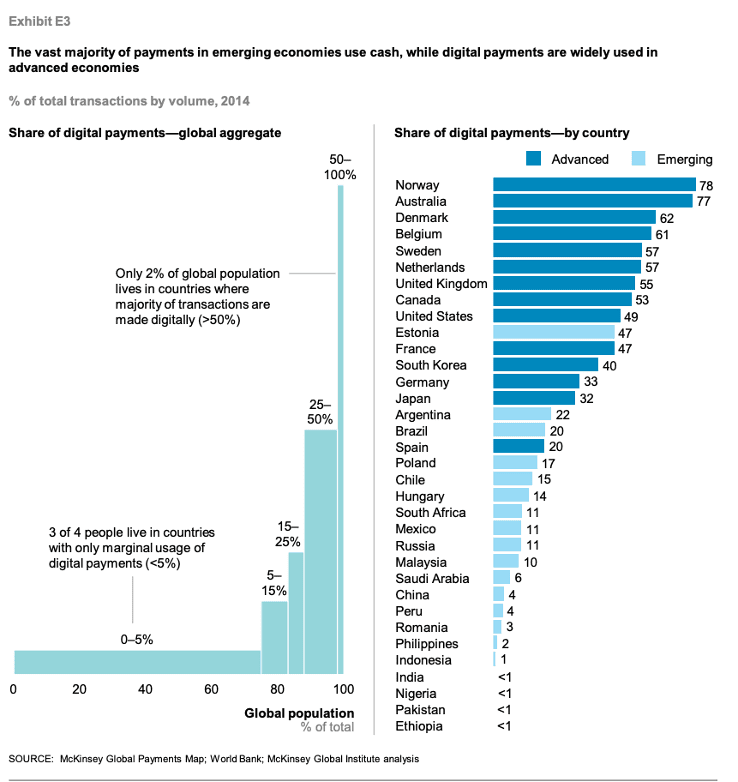

In developing economies, Individuals and businesses of all sizes overwhelmingly use cash, which makes up more than 90 percent of payment transactions by volume. This over-reliance on cash makes it difficult for financial service providers to gather the information needed to access the creditworthiness of potential borrowers, which further narrows the number of MSMEs that can access finance and credit.

Excessive cash payments also hurt both large and small companies in emerging markets, as the costs of handling cash become significant at scale. FMCGs and large distributors reportedly spend between 2 to 9 percent of their total revenue on managing and processing cash, while retailers and merchants lose 4.7 to 15.3 percent per transaction.

Digitizing payments is a transformational solution that can be implemented rapidly to reduce the credit gap as mobile phones and digital technologies continue to spread in emerging markets. Statistics show that 90 percent of adults in developing countries already have a mobile phone, and for small business owners in these economies, the mobile phone in the palm of their hands can redefine finance and be used to pay suppliers and distributors, accept customer payments, among many other use cases. Most importantly, adopting digital payments provides MSMEs with a data trail that can be assessed to provide credit history and collateralized to access advanced supply chain financing, loans, and other financial products.

However, despite the huge opportunity that digital payments seem to provide, getting individuals and small businesses to adopt it has not been easy. Digital financial service (DFS) providers have discovered that cash works well enough for most businesses in the informal sector; hence, adopting digital payments is not an attractive solution for MSMEs. To complete the digital transformation of payments in emerging markets, DFS providers must build platforms and products that put merchants first while addressing the financial, operational, and logistical pain points they experience daily.

RedCloud is closing the credit gap with the world’s first open commerce platform

RedCloud is helping close the MSME credit gap by building the world’s first open commerce platform. We remove the friction and the risk that is created by handling cash, speeding up the distribution process, and enabling merchants to trade directly with local and global brands.

RedCloud has also solved the problem of low merchant adoption rates by simplifying the logistics of digitalizing cash and providing incentives to drive user adoption and retention. We have partnered with hundreds of thousands of local cash deposit outlets and ATMs to enable merchants ‘upload’ their cash to the platform. With their cash digitalized, merchants can now connect and trade directly with national and global brands on the platform. We also provide instant access to digital products like phone credit, TV and Netflix subscriptions that can be sold in-store to their customers while earning a commission on each transaction.

As merchants use the open commerce platform to build up a trading profile, this data trail can be used to easily determine how their businesses are performing and allows financial services providers to offer affordable credit facilities – a safe and sustainable way to solve the $5 trillion credit gap.

Our CEO, Justin Floyd, says, “If we can bring merchants into the digital ecosystem and eradicate cash from the supply chain, there is potential to create a true ‘sell anywhere’ economy, where global and local brands can connect with any local merchant in any market. This can only happen if the commerce technology we build is open and accessible to all.â€

RedCloud ‘s vision is to reinvent commerce and empower over a billion new merchants in the world’s fastest growing economies to serve the 5 billion new middle-class customers that will be created by 2025. Contact us today to discover how RedCloud is helping merchants in emerging economies grow their businesses by up to 40% by enabling them to buy better, sell smarter, and pay simpler.