Today, across emerging markets, over 2 billion individuals and 200 million small businesses are excluded from accessing critical financial services, leading to high levels of inequality, and increased social and economic challenges. Micro, Small, and Medium Enterprises (MSMEs), which constitute over 90% of all businesses, and provide over 50% of the employment in emerging economies, cannot access the financial services they need to grow their businesses. The World Bank estimates that about half of all formal MSMEs lack access to formal credit, with an unmet financing need of $5.2trillion every year, and the gap is even larger when informal enterprises are considered.

This article discusses the importance of financial inclusion and how digital payments can help accelerate the rate of inclusion in emerging economies. The article also shows how RedCloud is driving the adoption of digital payments inthe world’s biggest product category by providing FMCG brands, distributors,and retailers with a revolutionary digital commerce platform.

Driving financial inclusion with digital payments

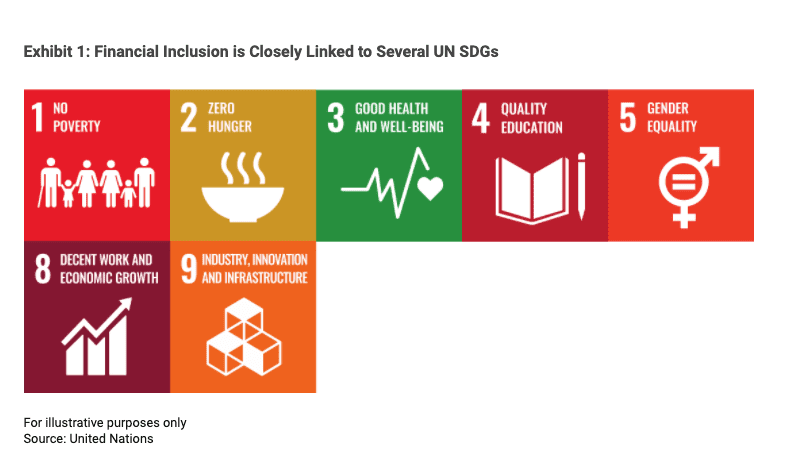

Research from the World Bank shows that increasing financial inclusion can drive economic development and increase the GDP in emerging markets by up to 14%. The United Nations has identified financial inclusion asa critical factor in achieving no less than 7 of the 17 Sustainable Development Goals, as financial exclusion remains a key enabler to the extreme poverty rates and lack of economic development.

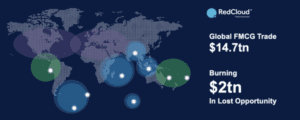

The overwhelming dominance of cash payments contributes significantly to financial exclusion, as low-income earners and informal MSMEs, who often constitute a large portion of the population, do not see any need to enter the formal financial system. Available data shows that over 90% of all consumer goods sold in emerging markets are paid for in cash, and annual cash payments are more than $19 trillion, or more than half of all global retail payments.

Digital payments can potentially reach over 1.6 billion new retail customers in emerging markets and reduce the existing $5 trillion credit gap by increasing the volume of credit accessible to businesses and individuals by $2.1 trillion. This will enable more small businesses to access the financial services they need to grow their businesses. The advantage of digital finance is not limited to individuals and MSMEs alone. Companies that build digital finance capabilities and provide digital payment solutions canaccess new revenue streams and increase revenues by $4.2 trillion.

Digital finance can also reduce the costs of doing business for both larger brands and smaller retailers, as cash payments cost consumer goods brands up to 20% of annual revenue, while small retailers lose up to 15% of their total revenue to cash handling and shrinkage. Evidently,there is a massive opportunity for digital financial service (DFS) providers,FMCG brands, and small MSMEs to increase revenues, reduce costs, and grow their businesses.

Digital payments are not catching on fast enough

While digital payments represent a huge opportunity in emerging markets and can help increase financial inclusion, it has yet to achieve widespread adoption. Millions of small businesses still pay for their goods in cash, and FMCG brands still require sales reps to collect those payments and transport them to reconciliation centers.

Digital payments have not caught on in emerging markets for several reasons, some of which are:

- Consumers still prefer cash payments: High levels of financial exclusion mean that many consumers can only pay for their goods in cash. Therefore, small retailers see no incentive in switching to digital payment solutions, as the burden of digitizing cash would fall on them.â€

- High transaction fees: While cash payments can costretailers up to 15% of revenue, these costs are often hidden. Digital payment platforms, on the other hand, charge transaction fees, which can seem expensive to the average retailer, as it appears that they are charged to use their own money.â€

- No single universal payment solution: There is often no universally accepted digital payment solution in the market, as multiple brands attempt to drive cash digitalization with different payment solutions. This makes it even harder for retailers to adopt any single solution when buying stock from multiple brands.â€

- Low digital and financial literacy levels: Financial exclusion levels are higher among informal retailers and merchants, and switching to digital payments often requires a lot of training and education.

To fully adopt digital payments and increase financial inclusion levels, we need a new industry standard in commerce payments that provides significant incentives for both brands,retailers, and consumers.

Digitalize cash in emerging markets with open commerce

Open commerce is a new type of commerce platform that revolutionizes trade across emerging markets. Unlike other traditional centralized digital commerce platforms, open commerce is built on decentralization and open trade principles to create a sell anywhere economy where small retailers can directly access the brands and products they need to grow their business.

RedCloud has built the world’s first open commerce platform powered by the world’s largest local payment network with over 2 million pay-in points across 100 countries. This allows retailers and merchants in the most remote locations to digitalize their cash and make digital payments, even without a bank account.Retailers can digitize their cash in any accepted pay-in point with no transaction fees deducted and then use the digital cash to access a wide range of products and services from global brands.

We have incentivized digital payments for retailers and small businesses in emerging markets by providing access to global brands and distributors, so they can order the products they need, when they need them, at prices they can afford.Retailers can also accept digital payments from customers, manage their stores digitally, and grow their businesses with our integrated marketing intelligence tool. They can also sell digital products to consumers in their stores and earn a commission on each sale.

By providing small business owners, many of whom are financially excluded from the formal financial system, with a reason to adopt digital payments and start trading on the open commerce platform, we are opening a new world of financial products and services. This includes a Buy Now Pay Later scheme that allows retailers to access the credit facilities they need to grow their business.

Schedule a demo with us to see how RedCloud has empowered over 270,000 retailers in emerging markets to start trading digitally and grow their businesses.