If you wanted to buy an expensive item that you ordinarily couldn’t afford, like a $300 leather jacket, how would you pay for it? While many people would pay with a credit card, more consumers are switching to Buy now, Pay Later (BNPL) services.

BNPL, just like credit cards, allows shoppers to spread the cost of a purchase over multiple (usually four) installments. However, unlike credit cards, most BNPL options are interest-free and don’t require credit checks, making them an attractive option for consumers.

BNPL services mainly target smaller consumer purchases but can potentially deliver the credit that retailers and small businesses across emerging markets desperately need. This article examines why BNPL is so popular and shows how it can be used to provide retailers in emerging markets with the credit they need to grow their businesses.

Why is Buy-Now-Pay-Later (BNPL) so popular?

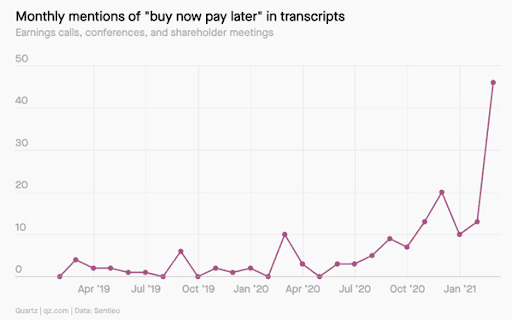

BNPL has become increasingly popular over the last few years, with reports showing that the BNPL industry is currently worth over $100 billion and accounts for over 2% of all e-commerce payments. The industry is also expected to grow to 15 times its current size to account for around $680 billion in transaction volume by 2025, or 14% of all e-commerce payments.

The rapid growth of BNPL is due to several factors, some of which include:

- A shift to e-commerce catalyzed by the pandemic: A UN report shows that the COVID-19 pandemic accelerated the adoption of e-commerce, with emerging market consumers making the greatest shift to online shopping. This made it easy for fintech companies that offer BNPL to expand their services rapidly.

- Low-interest rates and zero fees: Unlike other traditional forms of credit, BNPL typically charges zero or very low fees and interest rates, making them attractive to online consumers who were experiencing a squeeze on their finances.

- Doesn’t require existing credit checks: Most BNPL services don’t require credit cards or a credit check, making them ideal for consumers who aren’t eligible for credit cards or lack access to formal credit facilities.

Fintech brands, and other large companies, have recognized the huge opportunity BNPL presents and continue to enter the space, with Square acquiring BNPL provider Afterpay for $29 billion, and Apple announcing Apple Pay Later, its internal BNPL service launching by the end of 2022.

How Buy-Now-Pay-Later can help brands and retailers drive growth in emerging markets

John is a small retailer in Soweto who sells biscuits and receives orders when sales reps visit his store every month. However, the biscuits are in high demand and are usually sold out within two weeks of his order. Without direct access to the sales reps or visibility on the next delivery, he must wait for the next order and often turns customers away due to the biscuits being out of stock. John is also limited to the little cash he makes from his business as he doesn’t have a bank account. Without formal financial records, he cannot access loans to order more biscuits and grow his business, so he keeps losing customers.

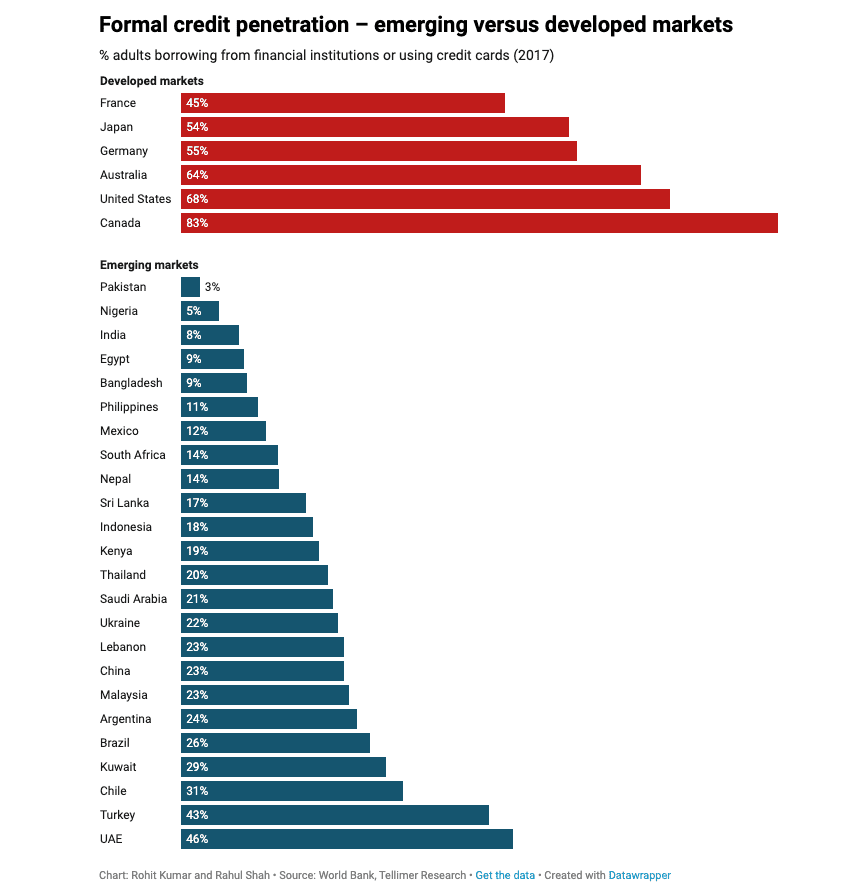

Across emerging markets, over 200 million estimated business owners like John, cannot access traditional forms of credit and are excluded from the formal financial ecosystem. The gap between the credit needed by these micro, small, and medium enterprises (MSMEs), and the credit available, is estimated to be above $5 trillion.

Available data shows that digital financial services like BNPL and digital payments can provide low-interest credit and financing options to over 1.6 billion small retailers like John and increase the volume of credit available in emerging markets by over $2 trillion. Like how existing BNPL services allow consumers to buy products and pay in installments, brands and distributors could allow retailers to buy more stock or other items needed for their stores, like refrigerators, and pay in installments.

However, making BNPL work for B2B retail in emerging markets would require digitizing the traditional supply chain. BNPL services work for consumers because more people are willing to shop for products and pay online. In contrast, most retailers in emerging markets don’t trade digitally, which is a significant barrier to providing access to the credit that they need.

Digitalizing the traditional retail supply chain in emerging markets has been a significant challenge for FMCG brands, despite numerous efforts to penetrate the largely informal market. FMCG brands and distributors have created mobile apps and digital payment platforms and even partnered with e-commerce providers to bring digital trading to small retailers with little success. This failure to penetrate the market has made providing credit to retailers at scale an almost impossible task.

Until now, that is.

Provide credit to retailers in emerging markets with Open Commerce

RedCloud has brought digital trading to retailers in emerging markets with the world’s first Open Commerce platform, Red101 Market. Open Commerce is a new, decentralized digital trading system where brands, distributors, and retailers can directly trade together on a single platform. While traditional e-commerce hijacks control of the entire supply chain and restricts brands and distributors from directly engaging with retailers, Open Commerce is focused on digitalizing the existing distribution chain and enabling brands and distributors to reach new and existing retailers.

We have also solved the low adoption rate of digital trading among retailers by providing a compelling value proposition that incentivizes retailers to start trading digitally. With Red101 Market, John can directly connect to brands and distributors to order products when he needs them and can pay online. In addition, Red101 Market has made digital payments easier than ever by building the world’s largest local payment network, so retailers like John in over 100 countries can walk into any of our 2 million pay-in points, digitalize their cash and pay for their FMCG products digitally, even without a formal bank account.

By providing a digital trading platform that retailers want to use, and an easy-to-use digital payment platform, brands, and retailers can now identify high-performing retailers and offer BNPL services. The payments can also be deducted automatically from the retailer’s wallets, making it easy for retailers to continue accessing even more credit.

With Open Commerce, brands can identify areas of high demand and provide high-performing retailers with targeted upsell and cross-sell offers that will drive sales growth and increase revenue.

Schedule a demo today to see how RedCloud can help your brand unlock the full value of your supply chain and drive sales growth by providing retailers with BNPL services at scale.

â€