For millions of businesses in emerging markets, cash remains the primary method of payment. It is used by consumers and businesses alike. The World Bank recently reported that over 50% of all retail payments are still made in cash. In today’s newsletter, we examine why cash payments remain so prevalent, despite the numerous efforts to replace them.

Let’s talk about money.

Cash remains a uniquely expensive and inconvenient way to do business. It reportedly costs retailers up to 15% per transaction, with cash handling costs for large consumer brands reaching up to 2% of total revenue.

This has led to concerted efforts by policymakers, businesses, and financial service providers, across emerging markets to replace cash with digital payments.

However, many of these attempts to digitize retailers’ payments and drive a cashless society have faced stiff resistance. For example, the Nigerian Government recently announced a cap on weekly cash withdrawals for individuals and corporations, with punitive fees levied on those who stray above the limits. This, in conjunction with the recent currency redesign in the country, forced citizens to remit all the cash in their possession but left them unable to withdraw hard currency.Â

According to the Nigerian Central Bank, these steps were meant to reduce the reliance on cash and increase the adoption of digital payments to make commerce flow and drive economic growth.

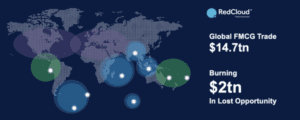

There is some merit to the proposition. Digital payments, if properly embraced, could present a huge untapped growth opportunity for the domestic economy and increase revenues for digital financial service providers by $4.2 trillion.

Given these incredible advantages, it’s important to ask…

…Why are cash payments still so prevalent?

The major reason why 90% of all retail payments across emerging markets are made in cash is simply because retailers prefer it!Â

Cash is convenient, instant, and, most importantly, accepted everywhere. At present, most digital payment solutions simply do not have the same widespread acceptance levels.

In addition, most retailers perceive cash as free, as cash handling costs are hidden and look insignificant, compared to the fees charged by digital payment platforms, which are visible and immediate.

The only way to drive the adoption of digital payments among retailers in emerging markets is to be significantly better than cash. While most digital payment initiatives have been positioned as a “better way to pay,†they are often inferior to cash, at least in the mind of the retailer.Â

Compelling value propositions that solve the key challenges of retailer and provide benefits beyond a replacement for cash must be built into digital payment options. For example, one of the biggest challenges small and medium-sized retailers face is the lack of access to working capital and credit facilities. Digital payments can provide trading records and detailed revenue data that support low-cost credit scoring, allowing retailers to access the credit they need to grow their businesses.Â

Another significant value proposition that can unlock the value of digital payments is building a more reliable supply chain for these retailers. Many of these retailers need direct access to distributors and brands and so cannot restock their shops with the products that their customers need, leading to a loss of revenue.Â

However, by building a trading platform that allows these retailers to access and order stock from their favorite brands and distributors in one place, they can be convinced to switch to a digital payments solution that seamlessly integrates into the trading platform. This way, they know their cash is being used directly to order stock, which will be delivered promptly, and help them keep their stores running.

Digitizing the supply chain and providing credit facilities are just a few incentives that can help increase merchant adoption of digital payments and unlock rapid economic growth.

What is needed now is greater market education that will nudge brands, distributors, and retailers towards open commerce technologies that provide the growth and freedom that they both want and need to drive consistent economic growth.