Emerging market and developing economies (EMDEs) make up 84% of the world’s population, but only contribute 37% of the Global GDP. In these markets, as many as 2 billion people and 200 million small businesses are entirely cut off from the formal financial system, lacking access to savings, investment, and credit facilities. The gap between the credit needed by MSMEs in developing economies and credit available is estimated at over $5 trillion. Closing this gap is crucial, as it will drive growth for MSMEs who provide over 80% of all full-time and help eliminate social and economic challenges among some of the poorest people in the world.

The solution to this problem is already in the hands of many – a mobile phone. Across emerging markets, mobile phone penetration is estimated to reach 80% by 2025, and more people will have mobile phones than bank accounts. Through digital finance, payments and other financial services delivered via mobile phones and the internet, we can help increase the rate of financial inclusion and sustainably provide over $2.1 trillion in credit to over 1.6 billion unbanked individuals and 200 million excluded businesses.

Digital finance can solve the financial inclusion problem

Digital finance and payments hold significant promise for everyone and can increase the GDPs of all emerging economies by 6% or $3.7 trillion by 2025 and create up to 95 million new jobs across all sectors of the economy. This is equivalent to adding a new economy to the world larger than all the economies of Africa.

Governments also stand to gain over $110 billion every year by reducing leakage through the shadow economy. Digital Financial Services Providers (DFS) can better assess credit risk for a wider pool of borrowers and make up to $4.2 trillion by expanding their customer base.

Over the last few years, there has been a rapid expansion of new technologies and innovations in the digital payments industry. With card and mobile-based payment solutions, more consumers and businesses in emerging markets can now access and use digital finance.

However, getting the financially excluded retailers to use digital payment solutions often means competing directly with cash, which is almost impossible. Therefore, to solve the financial inclusion problem and unlock growth for millions of unbanked MSMEs, DFS providers must first understand why cash remains king and build solutions that complement rather than outrightly replace cash.

Why cash remains king in emerging markets

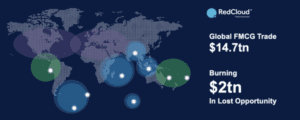

Cash remains the preferred payment method for small retailers in emerging markets. Available data shows that more than half ($19 trillion) of the $34 trillion global B2B retail payments made by Micro, Small & Medium Retailers (MSMRs) are done in cash. This is because cash is convenient, instant and universally accepted. Furthermore, no digital payment method offers similar versatility and universal acceptance, leading to lower adoption rates.

Different manufacturers and larger distributors across the retail industry often build their digital payment solutions or partner with other third-party DFS providers to eliminate the huge cash handling costs. However, the payment solutions often have low adoption rates of less than 10% because there is no real incentive for the retailer, who usually gets paid in cash by consumers. Retailers are then faced with the challenge of digitizing cash and learning how to use multiple payment platforms for the different brands or distributors they buy from.

Switching to digital payments will also require retailers to rethink their relationship with money, as many DFS providers charge fees on each transaction. This appears as a charge for spending their own money to the average retailer and is a thoroughly unattractive proposition.

There is not enough incentive for retailers to switch to digital payments in many cases, so they stick with cash. However, if we can build a new ecosystem that provides solid incentives for retailers, FMCG brands, and distributors to switch to digital finance, we can drive widespread adoption of digital payments, increase financial inclusion, and drive MSME growth. This is what RedCloud has built – a new system of commerce that unlocks the full value of the traditional supply chain in emerging markets and empowers everyone, from the smallest retailer to the largest FMCG brand to sell more and grow their businesses.

Solving the digital payments problem with open commerce

At RedCloud, we have taken the first step to drive rapid adoption of digital payments among small retailers by providing several compelling incentives. We built the world’s first open commerce platform that allows small retailers to directly access FMCG brands and order their stock in real-time. Merchants no longer have to wait for physical visits from sales reps and can pay digitally on the same platform.

Next, we built the world’s largest local payment network with over 2 million cash-in/cash-out (CICO) points across 100 countries. Retailers can walk up to any CICO agent and digitize their cash in minutes for free without needing a bank account. We realize that a strong cash-in/cash-out network plays a critical role in the transition from cash-based to fully digital payment systems, and retailers in emerging markets will only switch to digital payments if they can convert their cash into e-money and back again, as needed.

Finally, we created compelling use cases that incentivize retailers to digitize their cash and make digital payments. With our merchant app, retailers can sell digital products to their customers and make a commission on every sale, providing a new income stream. In addition, the digital trading profile generated as retailers continue to use the platform can be used to access credit risk and provide access to credit facilities even without a formal bank account.

With open commerce, financially excluded retailers in emerging markets can finally access the credit and financial services they need to grow their business.

Schedule a demo with us today to see how RedCloud is accelerating economic growth across the globe, and empowering over 270,000 retailers in emerging markets to trade digitally and grow their businesses by up to 40%.

â€